GST on Car Purchase & ITC Eligibility — Complete Guide for Indian Business Owners 🇮🇳

🚗 GST on Car Purchase & ITC Eligibility — Complete Guide for Indian Business Owners 🇮🇳

By Shahid Siddiqui | Business & Tax Awareness Series

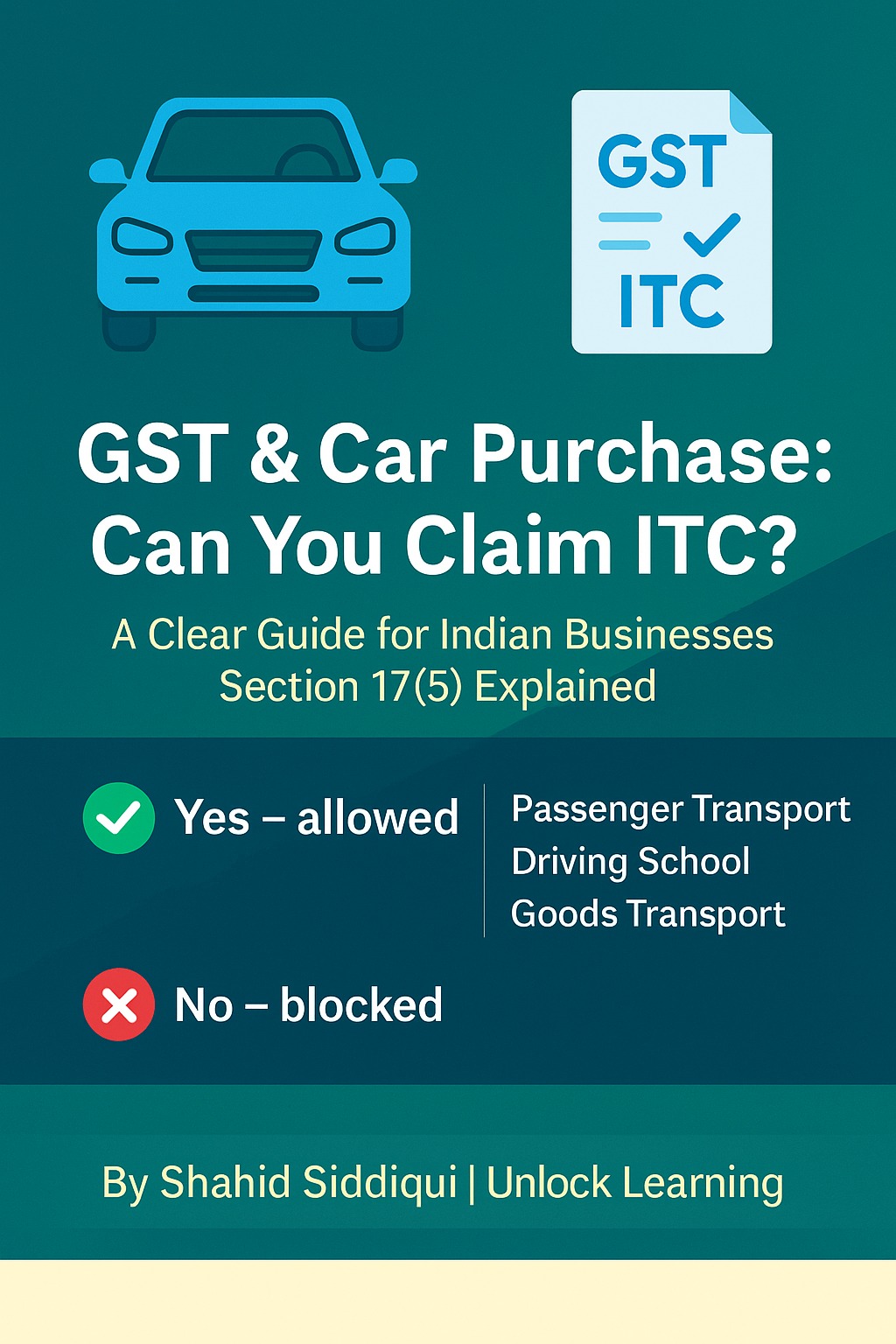

Buying a car for business use is common among entrepreneurs and companies in India. However, many people are confused about whether they can claim Input Tax Credit (ITC) on the GST paid while purchasing the car. The answer lies in Section 17(5) of the Central GST Act — popularly known as the Blocked Credit Rule. Let’s understand what this law means in simple terms.

Understanding Section 17(5): The Blocked Credit Rule

According to Section 17(5)(a) of the GST Act, businesses are not allowed to claim ITC on motor vehicles meant for personal or general business use. The government’s logic behind this is simple — cars are often used partly for personal purposes, so the credit cannot be given unless the vehicle is used for very specific business activities.

In short, ITC on car purchase is blocked, except for a few well-defined cases.

When ITC is Allowed

You can claim ITC on a car purchase only if the vehicle is used for:

-

Further supply of vehicles, such as in the case of car dealers or manufacturers.

-

Transportation of passengers, like taxi, cab, or travel service providers.

-

Driver training purposes, such as vehicles owned by driving schools.

If your business falls under any of these three categories, you can legally claim ITC on the GST paid for the vehicle.

When ITC is Not Allowed

For most regular businesses, ITC on cars remains completely blocked. This includes situations like:

-

Cars used for the personal or official travel of company directors, employees, or staff.

-

Vehicles used for office visits, client meetings, or general business purposes.

-

Cars that are used for both personal and business reasons.

Even if the vehicle is registered in the company’s name and payment is made through the business account, ITC cannot be claimed if it does not meet the specific exceptions mentioned in Section 17(5).

Commercial Vehicles and ITC

The rule changes when it comes to commercial vehicles such as trucks, lorries, dumpers, and other vehicles used for transporting goods. In these cases, the law allows ITC under Section 17(5)(a)(ii).

So, if your business involves logistics, manufacturing, or construction, you can claim GST credit on such vehicles, provided they are used solely for transporting goods.

Leased or Hired Vehicles

If a company hires or leases a vehicle for official use, ITC is generally blocked. The only exceptions are:

-

When the company itself is providing transportation services (for example, a travel agency).

-

When the company is legally required to provide transport facilities to employees, such as a factory providing bus service for workers.

Unless your business falls into these two categories, ITC on hired or leased vehicles cannot be claimed.

ITC on Repairs, Insurance, and Maintenance

The same rule also applies to expenses like insurance, repair, or maintenance of vehicles. If the main vehicle is not eligible for ITC, then any expenses related to it will also not be eligible.

However, if your business can claim ITC on the vehicle itself (for example, a taxi operator or travel company), then ITC on repairs and maintenance is also allowed.

Key Point to Remember

Even if you:

-

Purchase the car in your business name,

-

Make payment through your business account, and

-

Use the car for business meetings or office work,

you still cannot claim ITC unless your business falls under the exception list. GST law focuses on the actual purpose of usage, not just the ownership or payment method.

Pro Tip for Eligible Businesses

If your business is eligible for claiming ITC (like in travel, logistics, or driver training), make sure you follow proper documentation steps:

-

The invoice must be in the business name.

-

The vehicle registration should reflect commercial use.

-

Maintain a logbook or travel record to prove business use.

These documents will help if the GST department ever asks for verification.

Conclusion

In summary, ITC on car purchases under GST is allowed only for specific commercial purposes, such as passenger transport, driving schools, or goods transportation. For all other general or mixed-use cases, ITC remains blocked under Section 17(5) — even if the vehicle is purchased and paid for by the business.

So before buying a car under your company’s name, always evaluate whether your business type qualifies for ITC. This one check can save you from future tax disputes and unnecessary financial loss.

In short:

✅ ITC on car purchase — Allowed only for specific commercial use

❌ ITC on car purchase — Blocked for general business or personal use

🖋️ Written by Shahid Siddiqui

Tax & Business Awareness Series

#GST #TaxIndia #BusinessLaw #FinanceAwareness #ShahidSiddiqui